Opinion

Africa’s Economic Landscape Is Rapidly Evolving

By Dishant Shah

Africa’s economic dynamics are shifting at an impressive pace – and the continent is rewriting the rules of growth.

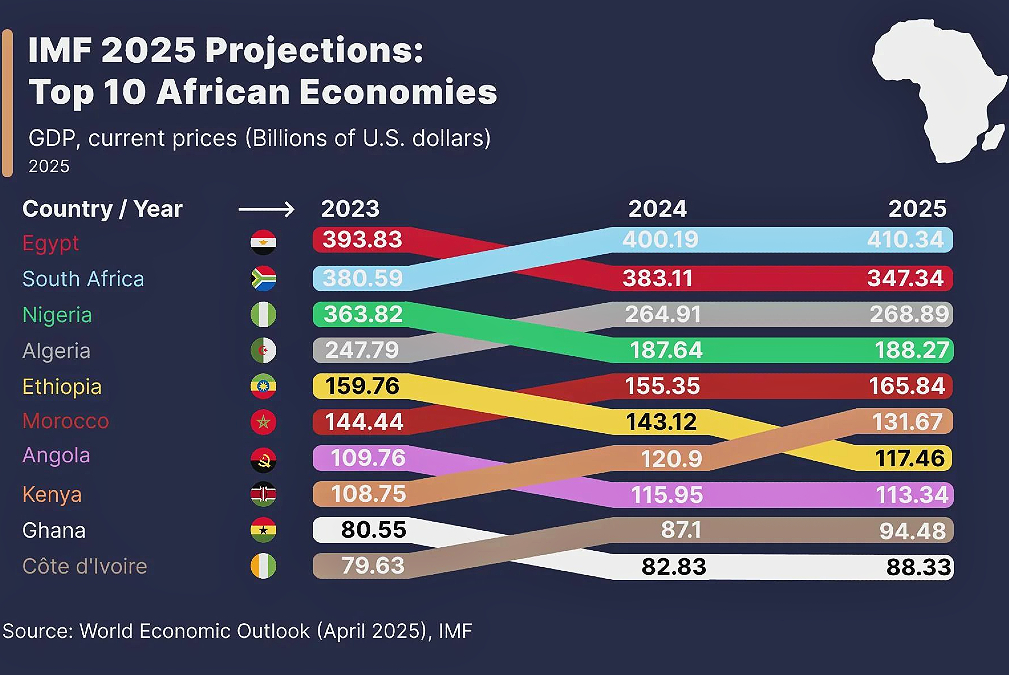

By 2025, South Africa is projected to overtake Egypt as Africa’s largest economy in nominal gross domestic product (GDP) terms, reaching an estimated US$410.34 billion. This marks a significant realignment in economic leadership on the continent.

Nigeria, once the region’s top economy, is expected to hold steady in third place with a gross domestic product (GDP) of US$268.89 billion. The slowdown reflects ongoing currency instability and deep-seated structural challenges that have hampered its full potential.

Egypt’s fall from first to second place between 2023 and 2025 underscores how quickly macroeconomic conditions – particularly exchange rate volatility and inflation – can reshape even the most promising growth stories.

Emerging Trends and Regional Shifts

But the narrative doesn’t end there.

Ethiopia, long recognized as one of Africa’s fastest-growing economies in real terms over the past decade, continues to build momentum. Its nominal GDP is expected to rise steadily from US$159.76 billion in 2023 to US$165.84 billion by 2025.

While it may not break into the top five just yet, Ethiopia’s investments in infrastructure and manufacturing signal strong long-term prospects.

Morocco and Algeria remain economic powerhouses, demonstrating resilience amid global uncertainties. Angola, meanwhile, is making a notable climb – projected to move into sixth place by 2025.

Despite fluctuations in global oil prices, Angola is showing signs of stabilization and modest diversification, allowing it to surpass Ethiopia in nominal GDP.

Further down the list, Kenya and Ghana are quietly gaining ground.

Ghana’s economic recovery is gaining traction, with GDP expected to rise from US$80.55 billion in 2023 to US$94.48 billion by 2025 – a promising rebound after years of financial strain and debt restructuring.

Côte d’Ivoire (Ivory Coast) also maintains its position among Africa’s top 10 economies, with a projected GDP of US$88.33 billion by 2025, reflecting consistent and stable growth.

Yet, one key dimension these figures don’t fully capture is the gap between nominal GDP and purchasing power parity (PPP). Economies like Ethiopia, Kenya, and Nigeria often rank significantly higher when measured by PPP, revealing a stronger base of domestic economic activity than nominal dollar values suggest.

For investors and policymakers, this alternative lens offers crucial insights into long-term economic vitality.

According to the International Monetary Fund’s World Economic Outlook, six of the ten fastest-growing economies in the world are African. But growth alone isn’t enough.

The future of Africa’s economic development hinges not just on size, but on resilience, productivity, and inclusiveness – and how effectively countries translate growth into jobs, opportunity, and sustainable development.

Toward a More Inclusive and Sustainable Future

Africa’s economic trajectory is anything but linear. It’s complex, dynamic, and brimming with potential – though not without its share of real challenges.

As we look at evolving rankings and shifting projections, the question isn’t just about who leads today.

It is about which nations are building the foundations for lasting, inclusive prosperity – and moving deliberately toward a stronger, more sustainable future.

What would it take for African economies to grow not only in scale, but in substance?

Dishant Shah is a partner at Legion Exim, a company specializing in facilitating the export of high-quality engineering products directly sourced from manufacturers in India to Africa. His areas of expertise include new business development and business management.