Opinion

Africa’s $1 Trillion Corporate Class: A Quiet Engine of Growth

At least 345 African companies now generate over $1 billion in annual revenue. Together, they represent a commercial force the world can no longer afford to overlook.

By Des H Rikhotso

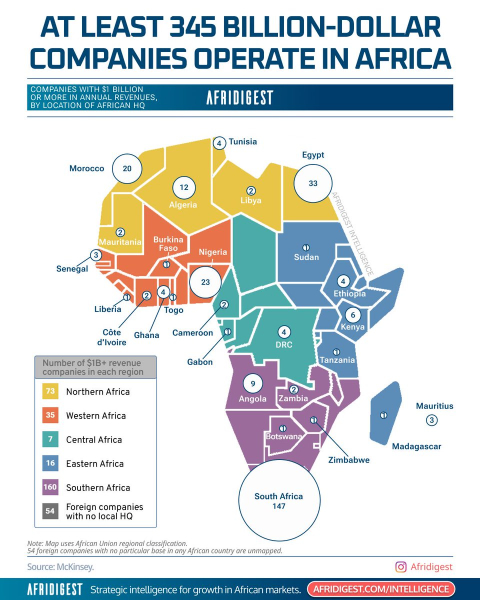

For too long, the dominant narrative around African business has fixated on what the continent lacks – infrastructure gaps, capital shortfalls, governance challenges. But a landmark report from McKinsey & Company quietly reframes that story with a single, striking data point: at least 345 companies operating across Africa each generate more than US$1 billion in annual revenue.

Collectively, they command a combined revenue exceeding US$1 trillion.

That is not a projection. That is today’s reality.

These firms – informally known as the “billion-dollar club” – are not multinational outposts or extractive foreign ventures. According to Semafor, roughly 230 of them were founded on African soil.

They are homegrown engines of commerce, and they are only getting started.

A Continent, But Not Yet an Equal One

The geographic distribution of this corporate wealth tells an important story about where Africa’s economic power currently resides – and where it has yet to fully emerge.

South Africa dominates, accounting for more than 40 percent of the billion-dollar club, with 147 companies headquartered there. Egypt follows with 43, Nigeria with 23, and Morocco with 20.

These four countries alone represent the overwhelming majority of Africa’s large-company ecosystem, creating a top-heavy landscape that reflects historical investment patterns, financial infrastructure maturity, and market size.

The concentration is both a testament to what these leading economies have built and a quiet indictment of the structural barriers that have prevented similar corporate champions from emerging more broadly across the continent’s 54 nations. Countries with comparable populations and natural endowments remain conspicuously underrepresented – a gap that is as much a policy challenge as it is a market opportunity.

Who Owns Africa’s Corporate Giants?

The ownership breakdown of these companies is a study in contrasts. Approximately 44 percent are publicly traded, offering investors some degree of transparency and access.

Another 40 percent are privately held, keeping their financial details – and their ambitions – largely out of public view. The remaining 16 percent are state-owned enterprises, a reminder that governments across the continent remain deeply entwined with commercial activity, for better and for worse.

That 16 percent figure deserves scrutiny. State-owned enterprises often serve political as well as economic objectives, and their inclusion in any measure of corporate vitality requires a degree of analytical caution. Revenue generated by a government monopoly is a fundamentally different animal from revenue generated in a competitive marketplace.

Six Sectors Drive Almost Everything

For all the diversity of Africa’s economies, its billion-dollar companies are remarkably concentrated in a narrow band of industries. Approximately 70 percent of total revenue flows from just six sectors: oil and gas, mining, retail and consumer goods, financial services, manufacturing, and telecommunications.

This concentration reflects Africa’s resource endowment and the sectors where capital has historically flowed most readily. It also signals a degree of fragility.

An economy whose corporate champions are overwhelmingly tied to commodities and extractive industries is an economy that remains vulnerable to price cycles it cannot control.

The good news – and there is genuine good news here – is that financial services and telecommunications represent a growing share of the mix. MTN and Vodacom, two of the club’s most recognizable names, are not digging minerals from the ground; they are building the digital infrastructure on which a modern economy runs.

Shoprite, Africa’s largest food retailer, and Bidcorp, the global foodservice giant with deep South African roots, demonstrate that consumer-facing businesses can achieve genuine scale on the continent. Sasol, the South African energy and chemicals company, represents the kind of industrial complexity that moves an economy up the value chain.

The Growth Imperative

Perhaps the most compelling figure in the McKinsey analysis is forward-looking. These 345 companies have the potential to grow their combined revenue by an additional US$550 billion by 2030 – a figure that, if realized, would represent one of the most significant expansions of corporate value on the planet over the next half-decade.

Between 2015 and 2021, Africa’s large companies grew revenues at an average annual rate of 4.9 percent. South African firms outperformed that benchmark, achieving 5.5 percent annual growth over the same period.

These are not trivial numbers. In a global environment of slowing growth and persistent economic uncertainty, they represent a genuine case for Africa as a destination for corporate ambition and investment capital.

The vehicle most likely to accelerate that trajectory is the African Continental Free Trade Area (AfCFTA), the sweeping trade agreement that came into force in 2021 and is gradually reshaping commerce across the continent. McKinsey specifically highlights intra-African trade as a critical growth lever for the billion-dollar club.

For companies that have historically built their franchises within national borders – or that have looked outward to Europe and Asia before looking inward to neighboring markets – the AfCFTA represents a structural shift of considerable magnitude.

The Narrative Must Change

The existence of a US$1 trillion corporate ecosystem in Africa will surprise many observers who have not been paying close attention. It should not. The continent is home to 1.4 billion people, a rapidly urbanizing middle class, and a median age of roughly 19 – the youngest population on earth. The demographic arithmetic alone argues for a dramatic expansion of corporate activity over the coming decades.

What the McKinsey data makes clear is that the foundation for that expansion already exists. The billion-dollar club is not a speculative construct; it is a documented commercial reality, generating revenue, employing workers, and building institutions across a continent that the world’s financial press has chronically underestimated.

The question is no longer whether Africa can produce billion-dollar companies. It already has – 345 of them. The question is how quickly the conditions can be created for the next 345 to emerge.

Des H Rikhotso is a seasoned C-Suite Multi-Industry (Automotive – OEM + Retail, Logistics, Oil & Gas, etc) business executive with 25+ years of Business Leadership Experience across the South, East and Western Sub-Sahara Africa Region. Based in Kampala, Uganda he serves as East Africa Region Country Director and Business Executive, driving Business Strategic Growth and Operational Excellence – contributing his Business Leadership Experience to the Region. Des has held Business Leadership roles at BMW Group Africa, Volkswagen Group Africa, Peugeot Motors South Africa, Toyota/Lexus South Africa, Lexus East Rand (Unitrans/CFAO), Nissan Group of Africa, G.U.D Holdings (Africa Exports Operations Division),The HDR Group of Companies and The Ezra Group of Companies (a Leading Uganda & East Africa Conglomerate). He holds Under-Graduate and Post-Graduate business degrees from the University of the Western Cape, Wits University (Wits Business School) and the University of South Africa.