Opinion

The Inheritance Problem: Africa Is Not Broken – Its Systems Were Built That Way

What the continent calls “development challenges” are, in many cases, the predictable outputs of infrastructure designed for extraction, not integration.

By Gregory September

When analysts speak of Africa’s structural deficits – its fragmented markets, its infrastructure gaps, its policy misalignments – they tend to frame these as problems to be solved. Rarely do they ask the more uncomfortable question: solved from what original design?

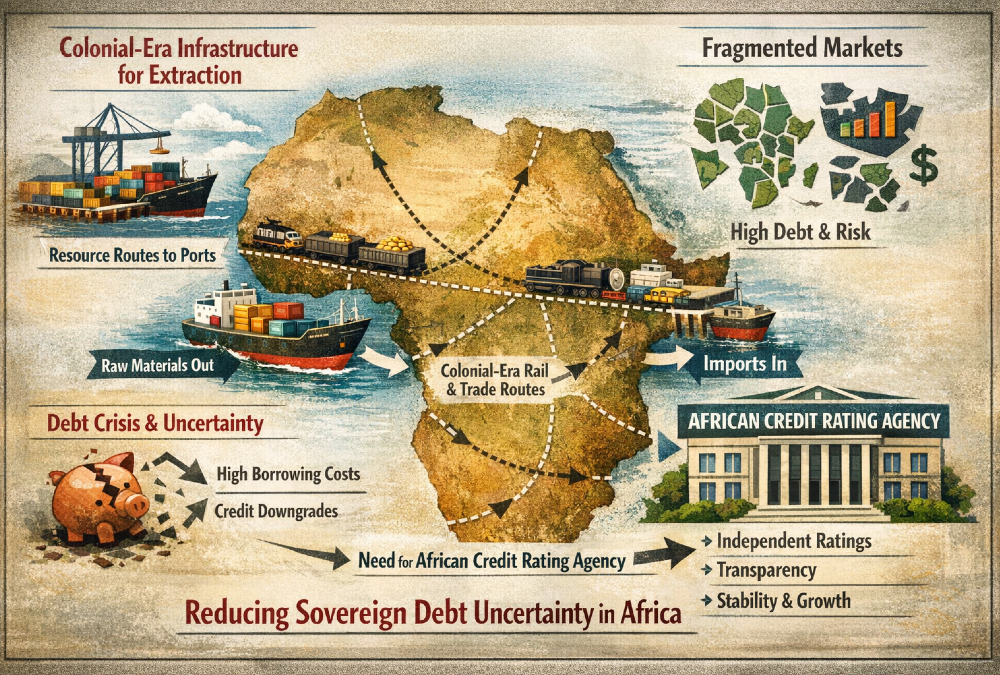

The borders that divide African markets were not drawn by Africans, nor were they drawn with African commerce in mind. The railways and ports that still define the continent’s logistics network were engineered to move raw materials outward, not to connect communities inward.

The regulatory frameworks layered on top of these colonial-era foundations were, in many cases, instruments of administrative control rather than economic coordination. These are not historical footnotes. They are the operating architecture of the present.

And yet the dominant vocabulary of African development treats their consequences – trade that cannot scale, infrastructure that terminates at national borders, policies that refuse to harmonize across regions – as if they were organic pathologies rather than inherited system constraints.

The distinction matters enormously. You cannot debug a system by treating its design as an accident.

The Price of Being Misread

Nowhere is this misreading more consequential than in sovereign debt markets, where Africa does not simply pay a risk premium – it pays an uncertainty premium. The difference is more than semantic.

Risk, properly understood, is quantifiable. It can be modeled, priced, and hedged. Uncertainty is something else: it is the condition that prevails when the data required to assess risk is absent, incomplete, or simply not trusted. Africa’s persistently elevated borrowing costs reflect all three.

The problem is structural and self-reinforcing. When data quality is weak, markets default to perception. When market liquidity is thin, volatility amplifies. When the risk models applied to African sovereigns are built on external frameworks – calibrated to different institutional environments, different political economies, different asset histories – context is systematically lost.

The market, confronted with what it cannot measure, charges for the discomfort. A perception problem becomes a pricing problem, and that pricing problem becomes a development constraint.

This is precisely why the debate surrounding an African Credit Rating Agency (AfCRA) deserves more serious attention than it typically receives in international financial commentary. The case for AfCRA is not that it would change Africa’s story. The case is that it would change the inputs – producing more granular data, supplying institutional context that external analysts routinely miss, and improving the visibility of African sovereign and sub-sovereign borrowers in global capital markets.

Reduce uncertainty at the measurement layer, and pricing begins to shift at the market layer. That is not a political argument. It is a systems argument.

The Harder Question

Two challenges, then, sit at the intersection of these issues – and neither is primarily a question of resources.

The first is whether Africa’s development agenda is, at its core, engaged in genuine problem-solving or in the sophisticated management of inherited dysfunction. There is a meaningful difference between designing institutions and infrastructure for an integrated continental economy and optimizing workarounds within a fragmented system that was never meant to cohere. The African Continental Free Trade Area represents an attempt at the former. Its implementation, in many corridors, still reflects the logic of the latter.

The second challenge is one of sequencing. Capital markets reprice slowly and, often, reluctantly. Even if an AfCRA were to materially improve data quality and sovereign transparency within the next decade, the question is whether that reduction in uncertainty would transmit to borrowing costs quickly enough to alter fiscal space in the near term – or whether markets would continue to anchor on legacy perceptions long after the underlying reality had shifted.

Neither question has a clean answer. But both demand that the conversation be elevated beyond the familiar registers of development aid and market access. The inherited architecture of African economic systems is not a background condition. It is the central variable. Until it is treated as such – in policy design, in capital markets, in the institutions that sit between them – the gap between Africa’s potential and its pricing will remain stubbornly, structurally wide.

Gregory September is a South African academic, author, and geopolitical analyst with extensive experience in government and Parliament. He is the founder and CEO of SAUP (Sustainability Awareness and Upliftment Projects NPC), which focuses on sustainability education and community development. He previously served as Head of Research and Development for the Parliament of South Africa. His work centers on sustainability, African geopolitics, and economic development, and he regularly contributes to analysis of global political and economic affairs.