Opinion

When Debt Becomes the Architecture of Dependence

Africa’s Eurobond surge is more than a balance-sheet problem. It is a structural challenge to sovereign economic decision-making – and the continent’s thinkers are demanding a reckoning.

By Wavinya Makai

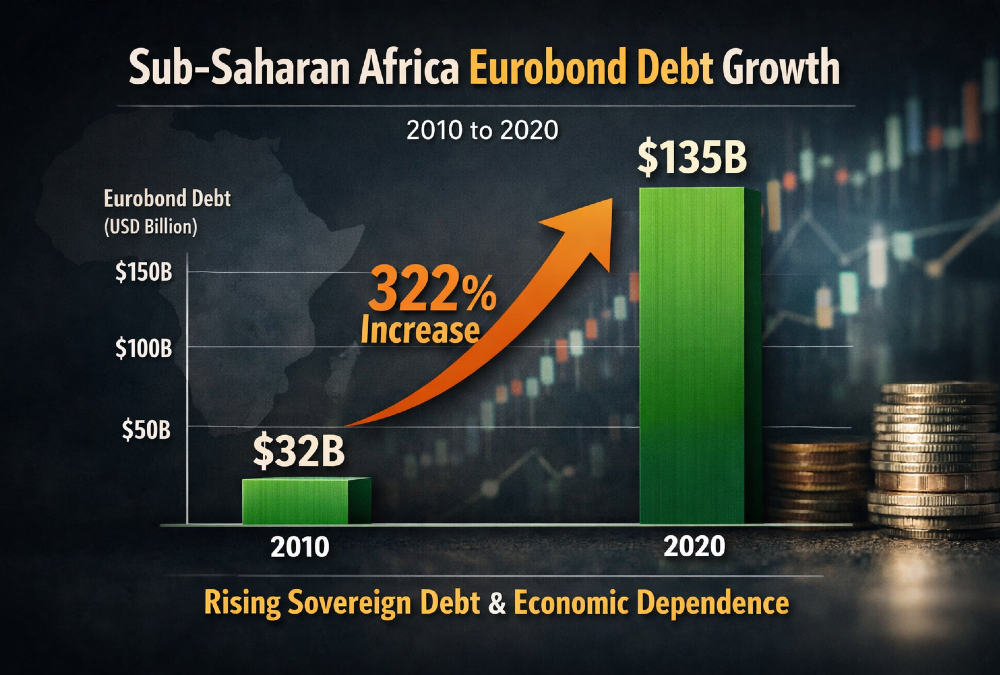

Consider a single data point. In 2010, Sub-Saharan Africa’s stock of Eurobond debt stood at approximately US$32 billion. By 2020, that figure had climbed to US$135 billion – a 322 percent increase in a single decade. In other words, the continent’s Eurobond obligations more than tripled in ten years.

That statistic, documented in the World Bank’s International Debt Statistics and underscored in Dossier No. 63 published by the Tricontinental Institute for Social Research in April 2023, is not merely a headline figure. It is a window into the political economy of our time.

The Seductive Grammar of Market Access

Eurobonds were introduced to African governments with the full apparatus of financial optimism. The language was seductive: market access, liquidity, development financing, investor confidence. The pitch was integration – a seat at the table of global capital markets, and with it, the resources to build the infrastructure a developing continent urgently needs.

Beneath that language, however, sits a more complicated reality. Eurobonds are denominated in foreign currencies – predominantly US dollars or euros – which means that the nations issuing them must service and repay that debt in currencies they do not print, do not control, and cannot devalue when economic conditions deteriorate.

The cycle that follows is frustratingly predictable:

- Governments borrow externally to finance infrastructure or stabilize public budgets.

- Global interest rates shift upward, or commodity prices fall, or both.

- Currency depreciation inflates the real cost of repayment.

- Debt servicing begins to crowd out spending on health, education, and industrial policy.

- Governments return to markets – or multilateral institutions – to refinance.

The result is a system in which development financing can quietly mutate into structural dependency – not through any single act of bad faith, but through the accumulated logic of a financial architecture that was never designed with borrower sovereignty as a primary concern.

When debt servicing crowds out spending on health, education, and industrial policy, financing stops being a tool of development and begins to look like a constraint on sovereignty.

The Structural Argument: Mkandawire and Nkrumah Revisited

The late Malawian economist Thandika Mkandawire – one of the most rigorous voices in African development studies – argued consistently that the continent’s recurring debt crises were never principally about fiscal mismanagement. They were, he insisted, about structural conditions: the narrow policy space available to economies that were integrated into global markets on unfavorable terms, with limited fiscal buffers and high exposure to external shocks.

That analysis maps onto an older and still-resonant framework. When Kwame Nkrumah articulated the concept of neocolonialism in 1965, he described it as a condition in which political sovereignty is formally intact but economic decision-making remains shaped – sometimes dictated – by external financial actors.

The flag is your own. The budget, however, is negotiated elsewhere.

The resonance of these frameworks is not a sign of ideological inflexibility. It is a sign that the structural dynamics they described have not fundamentally changed – only the instruments through which they operate.

Infrastructure Is Not the Problem. The Terms Are.

Let us be precise about what this argument is – and is not – claiming. It is not a case against infrastructure investment. Roads, ports, railways, and power systems are the arteries of economic transformation.

Africa’s infrastructure deficit is real, consequential, and costly. Any serious development agenda must address it.

The critical question is not whether to finance development. It is how development is financed, on whose terms, under what conditionalities, and – crucially – who ultimately carries the risk when external conditions shift.

When debt servicing begins to crowd out public investment – when countries spend more on interest payments to foreign bondholders than on their own citizens’ health and education – the instrument of development has become a constraint on it. That is not a polemical claim. It is, increasingly, an empirical one.

Economic Literacy Is Not Rebellion

There is a reflex, in some quarters, to dismiss these questions as ideological. To label structural critique as anti-market, or to treat any skepticism of capital market integration as a form of economic nationalism unbecoming of serious policymakers.

That reflex should be resisted – firmly and openly. Asking difficult questions about the architecture of global finance is not rebellion. It is responsibility. It is precisely the kind of analytical rigor that good governance demands.

Across the continent – from Nairobi to Lagos, from Accra to Johannesburg – a new generation of economists, policymakers, and civil society leaders is beginning to engage these questions with exactly that spirit: not from grievance alone, but from an insistence that the next cycle of policy choices be made from knowledge rather than illusion, and from negotiating strength rather than desperation.

The Deeper Question of Capital Control

Development, in any meaningful sense, is not simply about capital flows. Capital without conditions is rare; capital without consequences is a fiction.

The real question is who controls the terms on which capital moves – and, by extension, who shapes the development priorities of nations that depend on it.

That question has no tidy answer. Global finance is not a conspiracy. Its institutions are not monolithic, and its practitioners are not uniformly indifferent to development outcomes.

But systems do not need malicious intent to produce structural effects. They need only incentives that are misaligned with the interests of the most vulnerable actors within them.

The 322 percent increase in Sub-Saharan Africa’s Eurobond debt between 2010 and 2020 is not, by itself, evidence of exploitation. But it is evidence of a trajectory – and trajectories have destinations. Understanding where this one leads, and whether that destination is acceptable, is not optional.

It is the central economic policy challenge of the next decade for much of the African continent. The conversation has begun. It deserves to be had at full volume, with full rigor, and without apology.

Wavinya Makai is a Kenyan author, development strategist, and Pan-African scholar specializing in African economic sovereignty. Her work focuses on youth development, unemployment, and education reforms that cultivate innovators. She is the author of Capital Violence: The Economic War on African Dignity and holds a Master of Philosophy in Development Studies from the University of Cambridge. Makai has been featured as a development analyst on Citizen TV Kenya and is a frequent speaker on leadership and human rights.