Opinion

Africa’s Digital Divide Isn’t a Gap – It’s a Gold Rush

The numbers on the map tell two very different stories. The question is which one you choose to read.

By John Kourkoutas

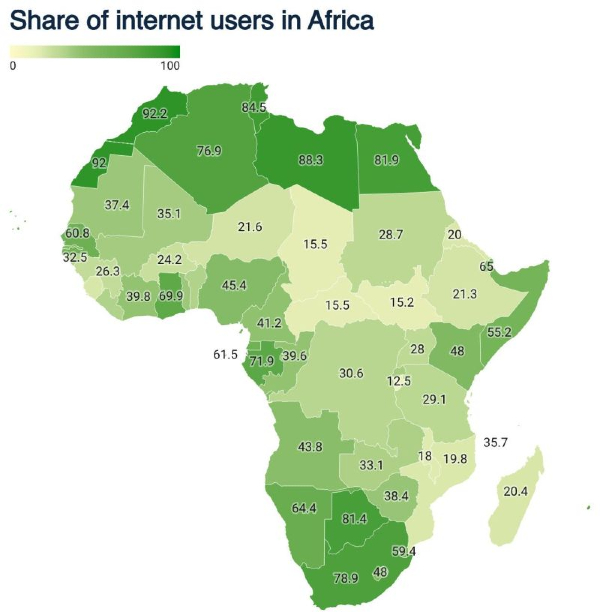

Consider the share of internet users across Africa, country by country. Along the northern rim and the south, the figures are striking in their modernity: Morocco at 92.2 percent, Libya at 88.3 percent, Egypt at 81.9 percent, South Africa at 81.4 percent.

These are penetration rates that would not look out of place in southern Europe.

Then look at the heart of the continent. The Democratic Republic of Congo sits at 30.6 percent. Tanzania at 12.5 percent. Burundi at 15.2 percent. The Central African Republic at 15.5 percent. Malawi at 18 percent. Mozambique at 19.8 percent.

Two Africas exist on the same map – one connected, digital, and rapidly assembling the infrastructure of a modern tech economy; the other with more than 80 percent of its population still entirely offline. Most analysts, scanning those numbers, reach for the word problem. They are reaching for the wrong word entirely.

The Lens Is Wrong – and It Is Costing Investors Dearly

There is a persistent failure of imagination among Western business strategists when they encounter low internet-penetration figures in sub-Saharan Africa. They see a small percentage and conclude they are looking at a small market.

That analytical error has already cost a generation of European companies their first-mover advantage in one of the fastest-growing digital economies on earth – and it threatens to cost the next generation the same.

The logic is straightforward once you apply the correct frame. Zambia’s internet penetration stands at 33.1 percent – a figure that, read in isolation, sounds modest.

But Zambia has a population of roughly 18 million people. That 33.1 percent represents approximately six million connected users: a digital market already comparable in absolute size to several Western European nations, and one expanding at double-digit annual growth rates.

Mozambique’s 19.8 percent sounds marginal until you recall that its population exceeds 34 million. Nigeria’s 45.4 percent penetration rate, applied to a population of more than 220 million, yields over 100 million people online – a connected population larger than the whole of Germany.

This is the essential arithmetic that Western market analysts consistently misread. Low percentages on a continent of 1.4 billion people still produce massive, and in many cases world-scale, absolute numbers.

And every single percentage point of growth represents millions of first-time digital consumers entering the economy simultaneously – new customers for e-commerce platforms, new users for digital banking, new audiences for content, new procurement channels for B2B suppliers.

What the Ground Actually Looks Like

Working across both of these Africas makes the contrast visceral in ways that no spreadsheet fully captures.

In Nairobi – Kenya’s internet penetration stands at 48 percent, representing roughly 27 million connected users – the co-working spaces are indistinguishable in energy and ambition from anything in Amsterdam or Berlin. Startups are building fintech platforms of genuine sophistication, products that do not merely replicate European models but improve upon them, engineered from the ground up for mobile-first, low-bandwidth, high-trust-deficit environments.

They are solving problems that European engineers have never had to think about – and in doing so, they are building solutions that will eventually travel in the opposite direction.

In Lusaka, WhatsApp functions as the operating system of commerce. Procurement, invoicing, customer service, supplier negotiation – entire business relationships are conducted through a single messaging application because it is reliable, universal, and already on every phone.

That is not a sign of a primitive business environment. It is a sign of a market that leapfrogged the infrastructural stages that slowed the West down, and built on what actually worked.

In Addis Ababa, where Ethiopia’s penetration rate of 28.7 percent would lead the incurious observer to dismiss the market entirely, the digital economy is not merely growing – it is accelerating. The relatively low penetration figure reflects a country of 130 million people in the early stages of a connectivity expansion that, by the arithmetic established above, will produce one of the largest new digital populations on the planet within this decade.

The Strategic Choice That European Companies Are Sleepwalking Past

The competitive logic for international businesses – particularly European ones – is not complicated, though it apparently requires stating plainly.

The alternative to African market entry is continued competition in economies where internet penetration has already reached saturation: markets where 90 percent or more of the population is online, where every major product category is dominated by entrenched incumbents, where customer acquisition costs are high, margins are compressed, and genuine growth requires displacing someone who has been there for decades. These are the markets in which European companies feel comfortable, because they are legible and familiar.

The markets that feel unfamiliar – the ones with the low penetration percentages and the infrastructure gaps and the regulatory complexity – are the ones where hundreds of millions of people are coming online for the first time, where brand loyalty has not yet been won by anyone, where the cost of acquiring a customer is still low, and where the compounding returns on early investment are, by historical precedent, extraordinary.

The companies that understood this logic in China in 2003, or in Southeast Asia in 2012, did not do so because those markets looked easy. They did so because they understood that the difficulty of entry and the scale of eventual opportunity are, in emerging digital economies, almost always proportional.

Africa in 2026 is not a problem to be solved at some later date when conditions improve. It is a window – measurable, time-limited, and currently wide open.

The only real question is how many more years of first-mover advantage Western companies are prepared to give away before they walk through it.

John Kourkoutas is business development expert that specializes in helping companies, export teams, and business leaders succeed in Africa’s dynamic and emerging markets.