Opinion

Africa’s Wealth Problem: The Value Chain Trap

The continent’s resource abundance is not in question. What is in question is whether African nations capture the wealth that those resources ultimately generate.

By Gregory September

Owning a mine does not make you rich. That may seem counterintuitive in a continent that sits atop some of the world’s most coveted deposits of cobalt, copper, lithium, oil, and natural gas.

Yet across Africa, a troubling paradox persists: extraordinary resource wealth coexists with extraordinarily limited economic returns. The reason is not difficult to find, though it is stubbornly difficult to fix.

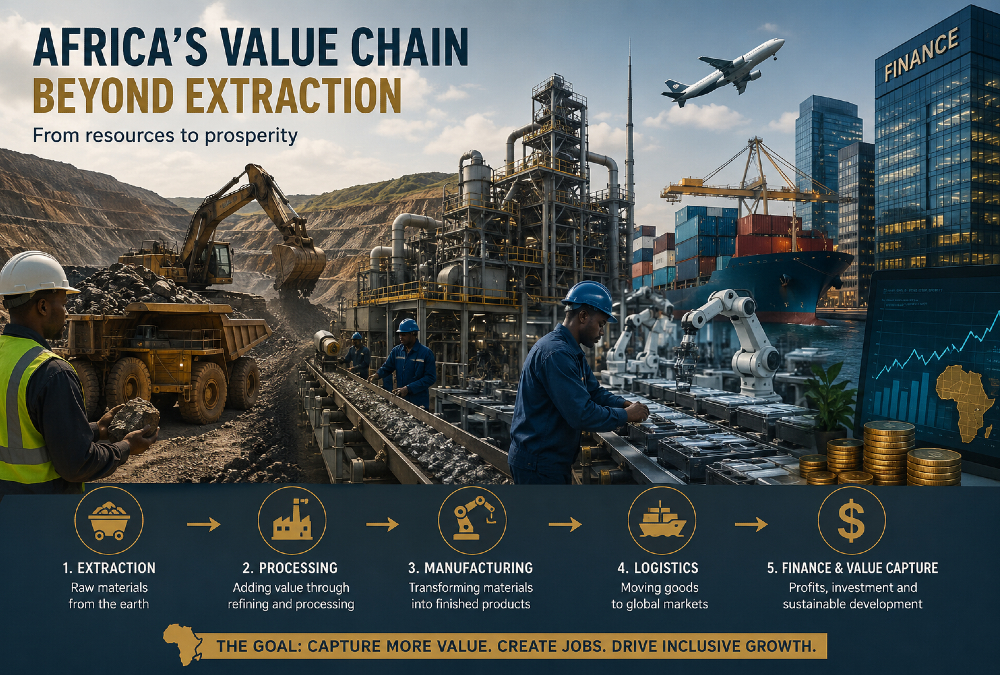

Africa’s most consequential economic challenge is not what it extracts from the earth. It is where it sits in the global value chain.

The distinction matters enormously. Extraction – pulling raw materials from the ground – is only the first, and often least lucrative, stage of a long industrial journey. The real value accumulates further along: in processing facilities, manufacturing plants, proprietary technologies, sophisticated logistics networks, and the financial systems that underwrite it all.

A ton of raw cobalt is worth a fraction of the battery cell it eventually becomes. A barrel of crude oil yields far less revenue than the refined petroleum products or petrochemicals derived from it. The gap between what Africa earns and what it could earn is, in large part, the gap between extraction and everything that follows.

This is not a new observation. Development economists have long warned about the “resource curse” – the paradox by which commodity-rich nations can suffer slower growth, weaker institutions, and greater inequality than their resource-poor peers.

But framing Africa’s challenge purely as a curse misses something important. The problem is not that resources are inherently destructive. It is that the global economy, as currently structured, rewards what happens after extraction far more than extraction itself.

Profits, capabilities, and durable competitive advantages are built downstream. And for most of the past century, that downstream activity has taken place elsewhere.

Leverage Without Influence

Africa’s geography reinforces this dynamic in ways that are rarely fully appreciated. The continent straddles some of the world’s most strategically significant trade corridors.

The Strait of Bab el-Mandeb, through which a substantial share of global container traffic passes, sits at Africa’s northeastern tip. The Cape of Good Hope remains a vital alternative routing for vessels avoiding the Suez Canal.

West Africa’s coastline anchors Atlantic energy supply chains. On paper, this positional leverage should translate into economic power. In practice, the translation has been incomplete at best.

The reason lies in a distinction that is easy to overlook: the difference between leverage and influence. Leverage is a structural fact – a geographic or resource-based advantage that exists regardless of what a country does with it.

Influence is earned. It requires institutions capable of converting structural advantages into negotiating power, investment, and long-term industrial development.

A country that controls a critical mineral deposit has leverage. Whether it captures the full value of that deposit – through refining, manufacturing, or technology development – depends on governance, infrastructure, regulatory capacity, and the political will to resist arrangements that lock in low-value roles.

History offers instructive contrasts. Norway discovered North Sea oil in 1969 and built one of the world’s most successful sovereign wealth funds, tight regulatory frameworks, and a domestic industrial base around it.

Many African oil producers have followed a different trajectory – one in which extraction contracts were signed on unfavorable terms, revenues were poorly managed, and little industrial capacity was built. The difference was not geology. It was governance.

Moving Up the Chain

The strategic imperative for African governments is therefore clear, even if the execution is genuinely difficult: move up the value chain. Several pathways exist, and a number of African nations are already pursuing them with varying degrees of success.

The most direct route is beneficiation – the domestic processing of raw materials before export. Zimbabwe and Namibia have both enacted policies restricting the export of unprocessed lithium and other critical minerals, seeking to force investment in local refining capacity.

The Democratic Republic of Congo, which produces roughly 70 percent of the world’s cobalt, has long exported the bulk of it as unrefined ore. A concerted push to build processing infrastructure could dramatically alter the economics.

Indonesia offers a useful precedent: its 2014 ban on raw nickel ore exports, though initially controversial, helped catalyze billions of dollars in domestic smelting investment and significantly increased the value captured locally.

A second pathway runs through regional integration. Africa’s industrial ambitions are constrained by fragmented markets – 54 countries, dozens of currencies, and trade barriers that make intra-African commerce more expensive than it ought to be.

The African Continental Free Trade Area (AfCFTA), which entered into force in 2021, represents the most ambitious attempt yet to address this. If fully implemented, it would create a single market of more than 1.4 billion people, enabling the economies of scale that manufacturing and processing require.

Progress has been uneven, but the framework exists.

A third pathway is technological leapfrogging. Africa’s relative lack of legacy industrial infrastructure is, in some respects, an advantage: the continent can invest in newer, cleaner, and more efficient technologies rather than retrofitting outdated ones.

The rapid expansion of mobile banking across East Africa – bypassing the traditional branch-banking model entirely – is the canonical example. Similar opportunities exist in renewable energy, precision agriculture, and digital logistics.

The Governance Question

None of these pathways can be navigated without addressing the deeper variable: institutions. The question of whether geography or governance matters more to long-run development is, at one level, a false choice – both clearly matter. But governance is the multiplier. It determines whether geographic and resource advantages are converted into durable prosperity or dissipated through mismanagement, corruption, and short-term thinking.

Strong institutions do not emerge overnight, and it would be patronizing to suggest that African governments simply need to make better choices. Many operate under severe fiscal constraints, face external pressures from creditors and trading partners, and contend with governance challenges that are in part legacies of colonial economic structures designed explicitly to facilitate extraction rather than development. The terms on which many African nations entered the global economy were not terms they negotiated freely.

That context matters. But it cannot become a reason for fatalism. The evidence from across the developing world is that institutional quality can be improved, that value chain upgrading is achievable, and that the rewards for doing so are substantial. Countries that have moved from commodity exporter to industrial economy – South Korea, Malaysia, Botswana in certain respects – did so through deliberate policy choices, sustained investment in human capital, and institutions capable of enforcing contracts and attracting capital on reasonable terms.

Africa is not short of resources. It never has been. What has been in shorter supply is the institutional capacity to convert those resources into lasting economic power – to move, in the language of development economics, from factor endowments to productive capabilities. The global energy transition is creating an urgent new opportunity: the minerals at the heart of batteries, solar panels, and electric vehicles are disproportionately concentrated in Africa. Whether this moment produces a different outcome than previous commodity booms will depend less on what lies underground than on the policy choices made above it.

Owning the mine is the beginning of the story. The question is who gets to write the rest of it.

Gregory September is a South African academic, author, and geopolitical analyst with extensive experience in government and Parliament. He is the founder and CEO of SAUP (Sustainability Awareness and Upliftment Projects NPC), which focuses on sustainability education and community development. He previously served as Head of Research and Development for the Parliament of South Africa. His work centers on sustainability, African geopolitics, and economic development, and he regularly contributes to analysis of global political and economic affairs.