Opinion

Africa’s Mobile Money Powerhouses: The Three Leading Regions

From East Africa’s entrenched dominance to West Africa’s explosive growth, the continent is rewriting the rules of financial inclusion.

By Des H Rikhotso

Africa does not merely participate in the global mobile money economy – it defines it. With Sub-Saharan Africa accounting for roughly two-thirds of all mobile money transaction value worldwide in 2025, the continent has long since moved past the “emerging market” framing that Western financial commentators reflexively apply.

What is unfolding here is not a developing story; it is a developed one – and three regions are driving it forward with remarkable speed and structural depth.

The data is unambiguous. Three regions – East Africa, West Africa, and Central Africa – are pulling ahead of the rest, each distinguished by its own economic logic, regulatory environment, and stage of maturity.

Understanding what separates them is essential not only to grasping Africa’s financial future, but to rethinking what modern banking can look like when it is built for the many rather than the few.

East Africa: The Epicenter That Set the Standard

No serious discussion of mobile money begins anywhere other than East Africa. This is where the category was invented, refined, and ultimately proven at scale.

Kenya’s M-Pesa, launched in 2007, was not merely a product – it was a paradigm shift that demonstrated, years before Silicon Valley would claim credit for “disrupting” finance, that a mobile phone and a SIM card could outperform a bank branch.

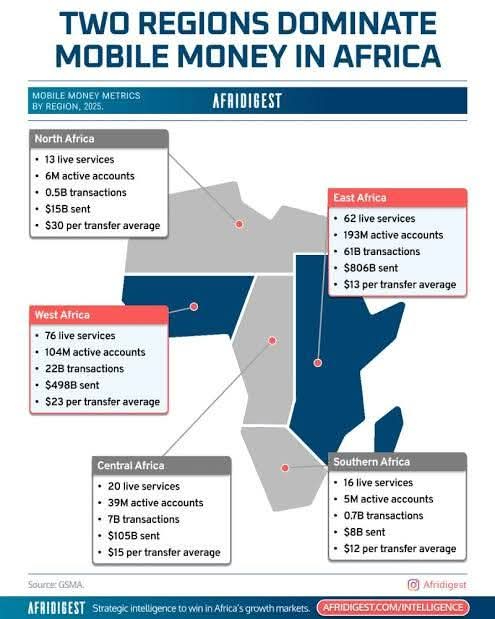

Nearly two decades later, East Africa’s lead has only deepened. In 2025, the region processed US$806 billion in mobile money transactions – a figure that would make the chief executives of many mid-sized commercial banks uncomfortable – across 537 million registered accounts.

It accounts for nearly half of all new active mobile money accounts opened globally that year. Kenya remains the gold standard for adoption, while Tanzania and Uganda have built substantial markets of their own, each with ecosystems sophisticated enough to support merchant payments, international remittances, and micro-credit.

What distinguishes East Africa is not simply volume, but depth. Mobile money here is not a parallel system running alongside conventional banking – in many communities, it is the primary financial infrastructure. That integration makes the region’s figures structurally durable, not a product of a passing consumer trend.

West Africa: The Region Everyone Should Be Watching

If East Africa represents mobile money’s established order, West Africa represents its most exciting frontier. The region has recorded the highest growth in registered mobile money accounts of any area on the continent, driven in particular by Côte d’Ivoire (Ivory Coast) and Ghana – two countries whose regulatory frameworks have created conditions exceptionally conducive to adoption.

Ghana, notably, ranks first globally for mobile money regulation – a distinction that reflects years of deliberate policy design rather than accident. The result is a market that is not only large but well-governed, offering the kind of consumer protections and interoperability standards that give both users and investors confidence.

Ivory Coast, meanwhile, has expanded rapidly across its population, leveraging francophone West Africa’s growing smartphone penetration to bring first-time users into the digital economy.

The numbers confirm the momentum. West Africa recorded US$498 billion in transaction value in 2025, with 517 million registered accounts – figures that place it firmly in second position globally, trailing East Africa in volume but matching – and in some metrics surpassing – it in growth velocity.

For those seeking to understand where the next decade of mobile money expansion will be concentrated, this is the region to study.

Central Africa: The Underappreciated Third Pillar

Central Africa receives considerably less attention in global financial coverage than its eastern and western counterparts, and that is an analytical error worth correcting. The region – anchored institutionally by the CEMAC bloc, the Economic and Monetary Community of Central Africa – has developed mobile money not as a convenience product for the connected, but as a primary financial tool for populations that have historically had almost no access to formal banking at all.

In this context, mobile money is not a feature of the economy; it is foundational to it. Cameroon leads the region in both account volumes and transaction activity, with Gabon emerging as a secondary market of note.

Together, Central Africa recorded US$105 billion in transaction value and 128 million registered accounts in 2025 – numbers that, while smaller in absolute terms than those of its neighbors, represent an extraordinary degree of financial access for a region long characterized by structural exclusion. The CEMAC region’s trajectory also deserves attention for what it signals about the next wave of mobile money growth: markets where penetration is still relatively low, but where the conditions – young populations, widespread mobile connectivity, and limited banking infrastructure – create powerful incentives for rapid adoption.

The Bigger Picture

Taken together, these three regions tell a story that ought to challenge some deeply held assumptions about where financial innovation happens and who benefits from it. The mobile money model that Africa has built – lean, accessible, and built around the realities of its users rather than the preferences of its institutions – has achieved what decades of development finance could not: genuine, scalable financial inclusion.

The world’s financial policymakers, development economists, and technology investors would do well to study these regions not as curiosities, but as blueprints. The question is no longer whether Africa’s mobile money model works. It manifestly does. The more pressing question is what the rest of the world is waiting for.

Des H Rikhotso is a seasoned C-Suite Multi-Industry (Automotive – OEM + Retail, Logistics, Oil & Gas, etc) business executive with 25+ years of Business Leadership Experience across the South, East and Western Sub-Sahara Africa Region. Based in Kampala, Uganda he serves as East Africa Region Country Director and Business Executive, driving Business Strategic Growth and Operational Excellence – contributing his Business Leadership Experience to the Region. Des has held Business Leadership roles at BMW Group Africa, Volkswagen Group Africa, Peugeot Motors South Africa, Toyota/Lexus South Africa, Lexus East Rand (Unitrans/CFAO), Nissan Group of Africa, G.U.D Holdings (Africa Exports Operations Division),The HDR Group of Companies and The Ezra Group of Companies (a Leading Uganda & East Africa Conglomerate). He holds Under-Graduate and Post-Graduate business degrees from the University of the Western Cape, Wits University (Wits Business School) and the University of South Africa.