Opinion

Africa’s Currency Disconnect: Why Your Money Crosses Borders Slower Than You Do

By Dr. Princess C. Mutisya

“Africa has 33 currencies, yet none is accepted anywhere on the continent. I fly from Nairobi to Addis Ababa, show my Kenyan shilling, and they ask, ‘What is this?’ But if I show the dollar, they say, ‘This is it.'”

This observation cuts to the heart of Africa’s most persistent economic paradox. This isn’t rhetorical flourish – it’s the daily reality of commerce across a continent whose combined GDP exceeds US$3 trillion.

The absurdity is striking. A businesswoman can board a flight in Nairobi and land in Addis Ababa in under two hours.

Her money, however, cannot make the same journey. It must first route through New York or London, converting through dollars or euros, accumulating fees and delays at every checkpoint. She crosses the border faster than her capital can.

This isn’t a story about currency prestige or the dollar’s dominance. It’s about infrastructure – or rather, its absence.

The Real Problem Isn’t the Dollar

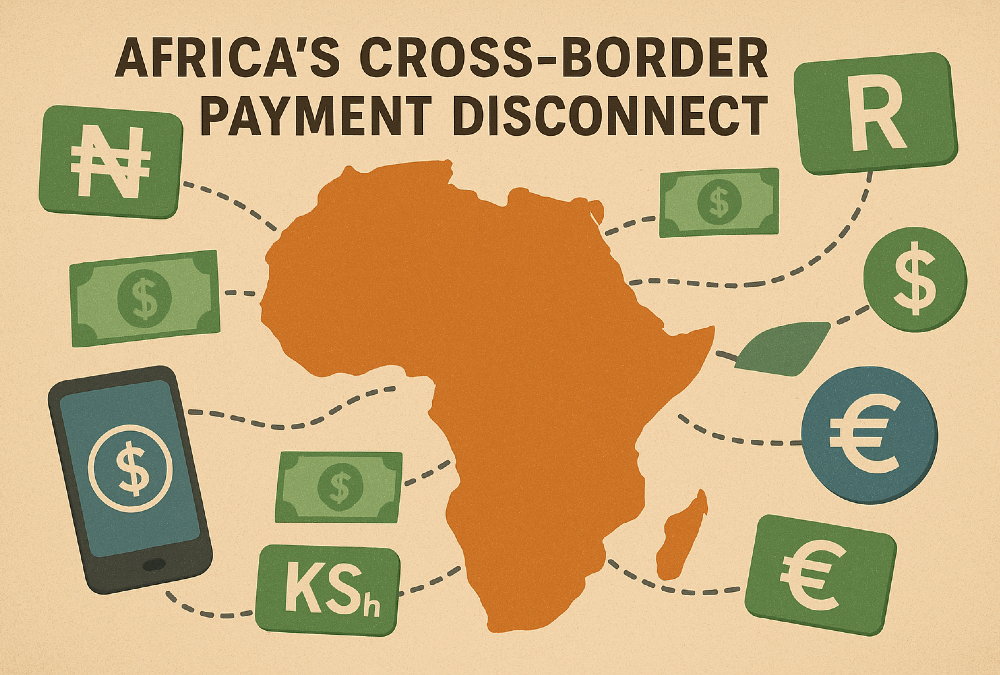

When more than 80 percent of intra-African transactions require foreign currency intermediation, the issue isn’t that African currencies lack value. The Kenyan shilling, the Nigerian naira, and the South African rand are perfectly functional stores of value within their borders.

The problem is that our financial systems don’t communicate.

Consider the mechanics: African currencies don’t have direct exchange pathways with one another. Payment systems operate in isolation, unable to process cross-border transactions without correspondent banking relationships routed through Western financial centers.

Regulatory frameworks move at different speeds, creating compliance nightmares for businesses attempting regional expansion.

The result is economic fragmentation masquerading as sovereignty. Thirty-three currencies create thirty-three walled gardens, each requiring separate navigation, separate relationships, and separate conversion costs.

The Cost of Disconnection

This fragmentation extracts an enormous toll. Businesses face unpredictable exchange rate exposure, not from market volatility but from inefficient routing.

Investors encounter opacity, unable to move capital fluidly across opportunities. Regulators operate with incomplete visibility into cross-border flows, hampering both oversight and policy coordination.

The African Continental Free Trade Area promised to unlock US$3.4 trillion in combined consumer and business spending. Yet that promise remains partially unfulfilled, not because of tariffs or trade barriers, but because the payment rails to support seamless commerce simply don’t exist.

A Tanzanian manufacturer who wants to sell to customers in Ghana shouldn’t need to establish dollar-denominated accounts and navigate correspondent banking fees. A Rwandan tech startup expanding to Senegal shouldn’t face weeks of payment settlement times.

These aren’t edge cases – they are the default experience.

Connectivity as Competitive Advantage

The solution isn’t to replace the dollar or create a single African currency – a political non-starter that confuses the symptom for the disease. The opportunity lies in building interoperable systems that allow existing currencies to transact directly with one another.

This is fundamentally about digital infrastructure: real-time payment networks, harmonized regulatory standards, and shared clearing mechanisms that treat the continent as a single economic space rather than 54 disconnected markets.

The technology exists. Regional payment systems like the Pan-African Payment and Settlement System show promise but lack universal adoption.

Mobile money platforms have demonstrated that Africans will embrace digital financial infrastructure when it works, M-Pesa processes more transactions than many traditional banks. The building blocks are present; they simply aren’t connected.

The Urgency of Now

Africa’s demographic dividend is arriving. By 2050, one in four people on Earth will be African.

The median age across the continent is 19. This isn’t a population waiting patiently for infrastructure to catch up – it’s a generation building businesses, creating digital solutions, and demanding systems that match their velocity.

Every day that African transactions detour through foreign currencies is a day that African markets remain harder to enter, harder to navigate, and harder to scale. It’s a competitive disadvantage baked into the architecture of commerce itself.

Connectivity has become the new competitiveness. The regions that thrive in the coming decades will be those where capital, goods, and services move with minimal friction.

Africa has the market size, the entrepreneurial energy, and the mobile-first infrastructure to compete globally – but only if its financial systems can communicate internally.

One Continent, One Market, One Payment Rail

The work ahead isn’t glamorous. It requires regulatory harmonization, technical standards, and political coordination across dozens of jurisdictions.

It demands that central banks, fintech companies, and regional bodies prioritize interoperability over institutional prerogatives.

But the alternative is to remain a continent where crossing a border is easier than sending money across it. Where economic potential is constrained not by human capital or natural resources, but by the systems – or lack thereof – that should enable exchange.

Africa is one integrated payment system away from unlocking its full commercial potential. The question is whether we will build systems that move as fast as our people do, or continue asking our currencies to seek permission from continents that don’t share our future.

The choice, ultimately, is whether Africa’s financial infrastructure will match the continent’s ambitions – or remain a relic of an era when borders mattered more than opportunity.

Dr. Princess C. Mutisya is a Strategic Legal Architect, author, and international business leader with more than 14 years of cross-border experience across Africa and the UAE. She is the Founder & CEO of CR Advocates LLP (Kenya) and CR Advocates Consultants LLC (UAE)among other leadership Roles. A recipient of Doctor of Laws (LLD) in International Legal Strategy and Doctor of Business Administration (DBA) in International Business & Global Transformation, Dr. Mutisya is an expert in international trade and investment law, advising governments, DFIs, and multinationals on investment law, sovereign frameworks, PPP structuring, Corporate Governance, trade facilitation, energy and infrastructure projects, real estate ventures, and private wealth structuring across Africa-GCC corridors. Beyond her legal and business enterprises, she is a global speaker and thought leader on economic diplomacy, policy innovation, and Africa’s emerging investment architecture.