Opinion

Africa’s Hard-Won Economic Gains Are Under Pressure

After a strong 2025, sub-Saharan Africa’s stabilization gains face fresh threats from Middle East conflict, rising commodity prices, and retreating foreign aid.

By Mark-Anthony Johnson

Sub-Saharan Africa entered 2026 in a position that would have seemed ambitious just a few years earlier. With regional growth estimated at 4.5 percent in 2025, policymakers across the continent had reason to believe that the painful stabilization programs of recent years – painful in fiscal terms, often more painful in social ones – were beginning to pay off.

That confidence has since been complicated by a convergence of external shocks that no government on the continent controls, yet every one of them must navigate.

The war in the Middle East has delivered a familiar but unwelcome jolt to commodity markets. Fuel and fertilizer prices have climbed sharply, squeezing household budgets and agricultural production simultaneously.

For nations still climbing out of the economic scarring left by the COVID-19 pandemic, the timing could hardly be worse. Social indicators that were already fragile – food security, poverty rates, access to basic services – now face renewed downward pressure.

Regional growth is projected to ease from 4.5 percent in 2025 to 4.3 percent in 2026 – a modest decline on paper, but one that masks considerable variation and significant downside risks in an environment of high global uncertainty.

Compounding the external shock is a retreat in foreign aid that analysts had warned about for years but which is now arriving with particular force. As wealthy nations direct resources toward their own fiscal pressures and geopolitical priorities, the safety nets that once cushioned the continent’s most vulnerable populations are thinning.

The IMF’s latest projections reflect this confluence of pressures with unusual candor.

Projected Real GDP Growth – Selected Sub-Saharan Economies (2026)

The headline figure of 4.3 percent conceals the striking heterogeneity that has long defined African economic analysis. Ethiopia and Uganda – projected at 9.2 and 7.5 percent respectively – are operating in a different register from South Africa, whose 1.0 percent forecast reflects the chronic structural impediments that have suppressed the continent’s most industrialized economy for over a decade.

Côte d’Ivoire (Ivory Coast) at 6.2 percent and Rwanda at 7.2 percent continue to reward years of institutional investment. Meanwhile, Angola and Senegal, at 2.3 and 2.2 percent respectively, illustrate how commodity dependence and fiscal fragility can conspire against even the most reform-minded administrations.

Nigeria at 4.1 percent sits close to the regional mean – a figure that belies the enormous policy challenge of managing a population of over 220 million through a period of currency adjustment, fuel subsidy removal, and external shocks. The country’s trajectory over the next 18 months will carry outsized significance for the region as a whole, given its economic weight and the spillover effects it generates across West Africa.

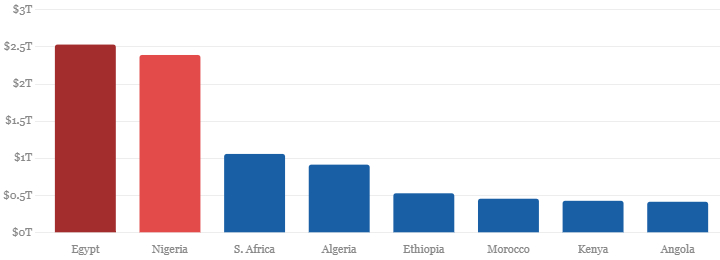

The GDP Ranking Shift – Africa’s Largest Economies By PPP 2026

Beyond the growth figures, 2026 has delivered a structural realignment in Africa’s economic geography that warrants attention in its own right. Egypt has displaced South Africa as the continent’s largest economy, measured by gross domestic product at purchasing power parity, with a figure of approximately US$2.53 trillion that places it 18th globally.

Nigeria follows at US$2.39 trillion – 19th in the world – reinforcing the degree to which sub-Saharan Africa’s economic center of gravity has shifted northward and westward.

Africa’s 18 Largest Economies by GDP (PPP) — 2026

| Rank | Country | GDP (PPP) | Global |

|---|---|---|---|

| 1 | Egypt | $2.53T | #18 |

| 2 | Nigeria | $2.39T | #19 |

| 3 | South Africa | $1.06T | #33 |

| 4 | Algeria | $0.92T | #39 |

| 5 | Ethiopia | $0.53T | #53 |

| 6 | Morocco | $0.46T | #58 |

| 7 | Kenya | $0.43T | #59 |

| 8 | Angola | $0.42T | #60 |

| 9 | Tanzania | $0.32T | #65 |

| 10 | Ghana | $0.32T | #67 |

| 11 | Côte d’Ivoire | $0.29T | #70 |

| 12 | DR Congo | $0.23T | #79 |

| 13 | Tunisia | $0.21T | #81 |

| 14 | Uganda | $0.20T | #82 |

| 15 | Cameroon | $0.18T | #85 |

| 16 | Zimbabwe | $0.14T | #92 |

| 17 | Sudan | $0.14T | #94 |

| 18 | Libya | $0.13T | #96 |

South Africa’s demotion to third – at US$1.06 trillion, roughly 60 percent of Nigeria’s PPP figure – is not a sudden event but the culmination of years of underperformance relative to its potential. Electricity supply failures, structural unemployment exceeding 30 percent, and institutional fragility have all extracted a compound toll that now shows clearly in the comparative rankings.

Algeria at US$915.8 billion and Ethiopia at US$530.8 billion round out a top five that would have looked quite different a decade ago.

Policy Imperatives

The IMF’s prescription is characteristically twofold: address the immediate shock while building medium-term resilience. In practice, that tension has rarely been comfortable for governments operating with thin fiscal buffers and populations whose patience with austerity has natural limits.

The near-term challenge is to cushion the impact of rising food and fuel prices without destabilizing the progress achieved on inflation and debt sustainability. The medium-term imperative is to reduce vulnerability to precisely the kind of external shocks that 2026 has delivered – through diversification, domestic revenue mobilization, and investment in agricultural productivity.

The downside risks are, by the IMF’s own assessment, significant. A further escalation in the Middle East, a sharper-than-expected slowdown in China, or a renewed tightening of global financial conditions could each push outcomes well below the baseline.

For a region where the baseline is already below the growth rates needed to absorb rising working-age populations, the margin for error is uncomfortably slim.

What the numbers ultimately describe is a continent that has done more than many give it credit for – and which now needs the rest of the world to do its part, or at least to stop making things harder.

Mark-Anthony Johnson is the founder and CEO of JIC Holdings, a global asset and investment management firm founded in 2009. With over 30 years of experience and strong ties to Africa, his investments span mining, infrastructure, power, shipping, commodities, agriculture, and fisheries. He is currently focused on developing farms across Africa, aiming to position the continent as the world’s breadbasket.