Business

Fintech – Changing the face of banking in Africa

By Eugene Yiga

Digital disruption has brought essential financial services to millions of people in Africa, where the traditional architecture of banks, cards and transfer services has been difficult to develop. We take a look at the start-ups shaking up the space. Mobile penetration in sub Saharan Africa is expected to increase from 52 percent in 2012 to 79 percent in 2020, according to a report from research and consulting company Frost & Sullivan.

This means that about 800 million Africans will have a cellphone.

Given the increasing availability of cheap smartphones, African mobile broadband connections were expected to quadruple from the 2012 figure to 160 million last year. All this points to many opportunities for FinTech companies that specialize in payments, lending, financial management, and other services.

Payments Nomanini, which means “Anytime” in Siswati, is a South African-based enterprise payments platform provider that enables transactions in the cash based informal retail sector.

“With our end-to-end solution designed for informal market environments, enterprise prepaid distributors are able to bolster their distribution channels, add to their portfolio of transaction services, increase their access to informal market consumers, and efficiently monitor micropayments and services via a scalable cloud-based platform,” explains chief executive Vahid Monadjem.

The company creates rugged point-of-sale terminals for use in places that have low cellular reception and unreliable electricity. The platform can handle sales of different virtual goods like airtime and electricity.

There are also online web management tools that provide real-time business intelligence data. Another leading company in the payments arena is Snapscan, which is also from South Africa.

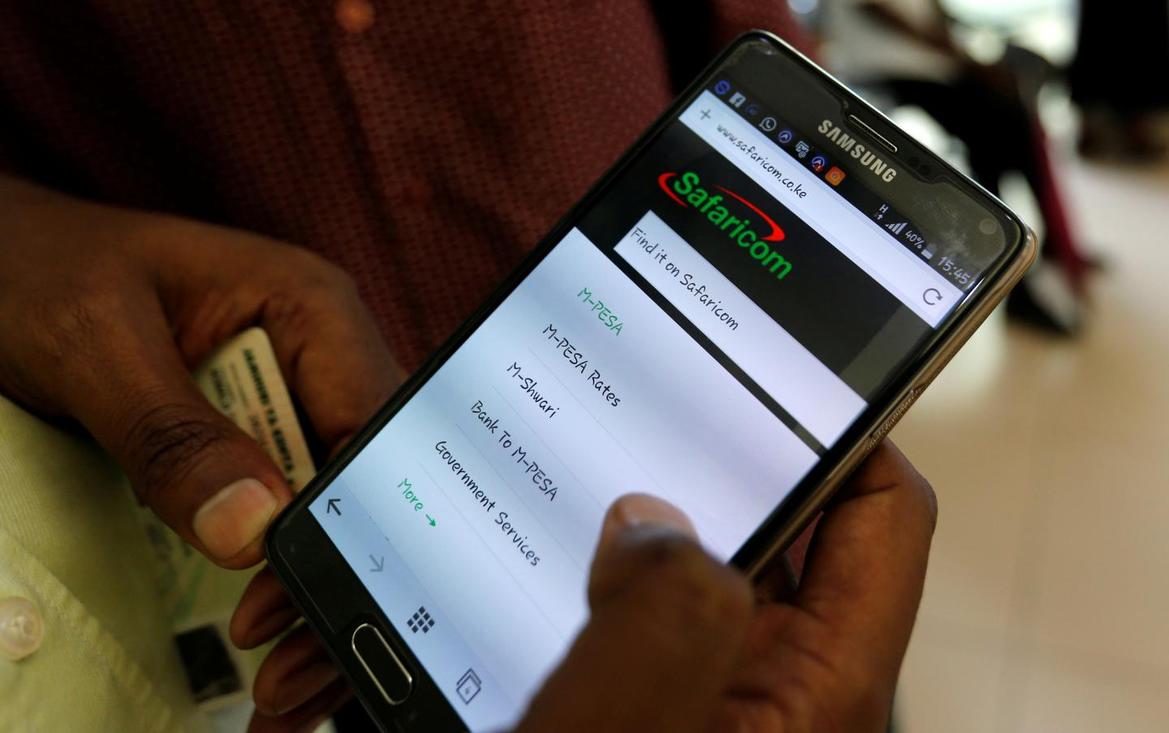

It has over 20,000 merchants and uses a smartphone app that supports credit cards, most debit cards from local banks, and 3D secure-enabled international bank cards too. So, instead of standing in a line or waiting for a credit card machine so that you can pay for your coffee, users scan a code with their phones. The app also lets users pay when shopping on their phones, settling monthly bills, or buying at a market. A third company that succeeds in this area is Kenya’s M-Pesa.

This mobile based money transfer, financing and micro-financing service was launched in 2007 by Safaricom and Vodacom, the largest mobile network operators in Kenya and Tanzania.

Users can deposit and withdraw money; transfer money to other users and non-users; pay bills; buy airtime; and transfer money between the service and a bank account. In Kenya, M-Pesa had about 17 million registered accounts in 2012.

The service has now expanded to Afghanistan, India and Eastern Europe. A company that offers a mobile money lending service is GetBucks. Founded in South Africa in 2011, it has helped 212,500 people in 9 countries with short-term financial needs. The simple sign-up process takes about 10 minutes, making it a quick and easy way for people to fund their needs.

Every time a borrower repays a loan, their “trust score” changes.

This gives them access to better deals in the future. Another company that gives access to money is InVenture, whose offices are in Kenya and the US.

It uses an Android platform to collect thousands of data points per customer, build a real-time credit score, determine loan terms, and disburse loans in less than a minute.

InVenture has disbursed millions of dollars in credit in East Africa and is rapidly expanding throughout Africa and Asia.

Lastly, South Africa’s 22seven is a free app that helps users manage their money more easily and invest it more smartly. By using the latest insights in behavioral psychology, the company is able to understand how we think and act when it comes to money.

It then combines this with the latest technology to help “nudge” people in the right direction.