Opinion

Why Africa Exports Potential and Imports Value

The continent does not only lose wealth at the port. It loses power along the value chain.

By Daki Nkanyane

Every day, Africa ships out pieces of its future.

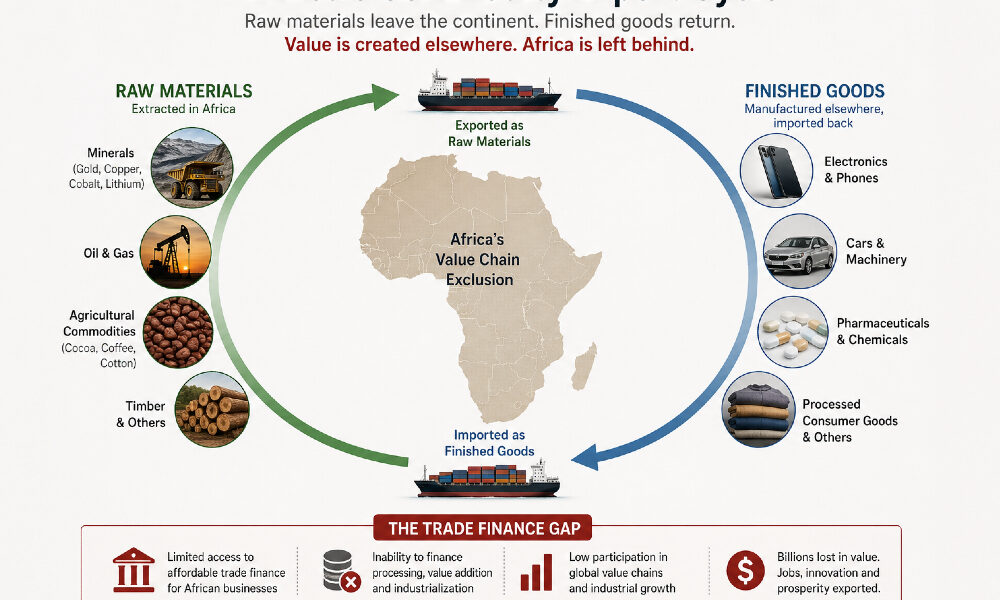

Those pieces leave through ports in the form of minerals, crude oil, unprocessed agricultural produce, and other raw materials – in bulk, in container loads, in tanker volumes, in impressive export figures that often flatter national accounts while concealing a deeper weakness. Then, after the long journey outward, much of that same value returns to the continent in another form: refined, packaged, branded, financed, patented, and priced at a premium.

What left as resource re-enters as dependence. This is one of Africa’s great paradoxes.

The continent is described as rich because it has what the world needs. And that is true, in part. Africa remains central to global supply chains in minerals, energy, agriculture, and strategic raw materials.

Yet the more uncomfortable truth is that being essential to someone else’s production system is not the same as being powerful within your own. Africa’s total merchandise trade rebounded strongly in 2024 to approximately US$1.5 trillion, but the continent still accounted for only 3.3 percent of global exports.

Afreximbank has stated plainly that moving away from commodity dependence remains central to deeper industrialization and greater value-chain participation.

That single fact should disturb us.

A continent so vast, so richly endowed, so demographically significant, and so strategically positioned in a changing world still occupies only a thin layer of global export power. That is not because Africa is absent from the global economy. It is because Africa is present in it – too often on subordinate terms.

We do not only export goods. We export unfinished advantage.

This is the part of the economic story that too many speeches still refuse to confront with genuine seriousness. Africa’s problem is not merely that it exports raw materials.

Many countries export commodities. The deeper problem is that Africa has too often failed to control what happens after extraction, after harvesting, after primary processing, after shipment.

The real money, the serious jobs, the technological learning, the mastery of standards, the premium branding, and the industrial leverage accumulate further downstream. That is where value thickens. That is where power settles.

And that is precisely where Africa remains too thin.

The Commodity Trap

UN Trade and Development’s latest commodity-dependence work reveals just how entrenched this pattern remains. An economy is considered commodity dependent when more than 60 percent of its merchandise exports are commodities; during 2021–2023, 95 of 143 developing economies met that threshold.

UNCTAD warns that such dependence weakens resilience and heightens exposure to price volatility and external shocks. Africa is not alone in this pattern, but it is one of the regions where the consequences are especially costly – because the development needs are so great and the upside from value addition is so large.

That is why Africa does not merely lose money at the point of export. It loses negotiating strength across the entire chain.

A country that exports cocoa beans but imports chocolate is not simply missing out on margins. It is missing out on design, food science, packaging, logistics expertise, market intelligence, retail positioning, brand ownership, and the ability to turn agricultural output into industrial depth.

A country that ships lithium or cobalt in raw or low-value form without capturing enough processing, component production, or adjacent manufacturing is not just losing revenue. It is surrendering entry into the industries that will define the next generation of global power.

UNCTAD has been increasingly explicit on this point in its work on critical minerals: the opportunity for developing countries – especially in Africa – lies not only in extraction but in processing and value addition that create jobs, build capability, and strengthen resilience.

In other words, the issue is not trade alone. It is position.

Position inside the chain determines whether a country is price-taker or price-maker, labor reservoir or skills hub, extraction site or industrial node, transport corridor or production platform. Africa has lived too long at the lower, thinner, more vulnerable end of too many global chains. We sell what the world transforms. We dig what others design around. We harvest what others brand. We host the raw material but too rarely command the ecosystem.

Movement Without Conversion

This is why the continent can appear busy without becoming strong.

Containers move. Revenues arrive. GDP rises in select quarters. Commodity booms briefly lift fiscal moods. Yet none of that automatically produces structural change.

If the chain remains externally controlled, if domestic suppliers remain shallow, if manufacturing remains fragile, if logistics are unreliable, if trade finance is scarce, and if industrial policy remains rhetorical, then export growth can coexist comfortably with underdevelopment.

That is the African discomfort: movement without conversion, extraction without compounding, trade without thickening.

The world does not reward raw participation equally. It rewards strategic placement. UNCTAD’s March 2025 trade update makes this even clearer by highlighting the damage caused by tariff escalation: many importing countries keep tariffs lower on raw materials but higher on processed and finished goods, deliberately reinforcing dependence on primary exports and making it harder for developing economies to climb into manufacturing and higher-value segments of supply chains.

So the task is harder than many African policymakers admit.

It is not enough to say that Africa must add value. Everyone says that now. The real question is whether Africa is building the institutional stamina to do so under adverse conditions.

The path from raw export to high-value participation is not a motivational journey. It is a systems journey. It requires energy reliability, transport efficiency, customs intelligence, standards infrastructure, technical training, patient capital, procurement discipline, market coordination, and states capable of thinking beyond extraction royalties and election calendars.

That is why value addition is not a slogan. It is an architecture problem.

The Importance of the Middle

Too often, African countries approach export transformation as though they can leap from the pit to the pinnacle without building what lies in between. They announce grand ambitions in batteries, agro-processing, pharmaceuticals, textiles, digital industries, and industrial parks, while neglecting the slower work of supplier development, logistics reform, machine maintenance ecosystems, industrial skills, standards certification, and medium-sized firm scaling.

Yet value chains are not conquered by aspiration alone. They are built through sequencing.

Africa must become far more honest about the middle.

The middle is where factories become competitive. The middle is where standards are learned. The middle is where local firms stop being symbolic and start becoming dependable. The middle is where an economy develops the unglamorous but indispensable habits of industrial seriousness.

Countries do not wake up one morning to find themselves integrated into higher-value trade. They build their way there through repeated competence.

That is one reason the continent’s manufacturing footprint remains so small relative to its scale. UNIDO’s 2025 Africa factsheet notes that in 2024, Africa accounted for 3.2 percent of global GDP but only 2.0 percent of global manufacturing value added.

That gap tells a story far larger than any statistic can capture. It tells us that Africa still consumes more world-making than it produces.

A Continent at a Crossroads

And yet the answer is not despair. The answer is design.

For the first time in a long time, the continent possesses ingredients it did not previously hold in sufficient combination. The African Continental Free Trade Area (AfCFTA) offers a continental market logic that can support regional value chains – if implementation deepens.

Intra-African trade grew by 12.4 percent in 2024 to US$220.3 billion, according to Afreximbank. That matters not only because of the figure itself, but because regional trade is often more supportive of industrial diversification than the old extractive trade patterns with distant markets.

Afreximbank also points to the Pan-African Payments and Settlement System (PAPSS) in reducing reliance on external currencies and improving payment efficiency – both of which matter greatly if African firms are to trade with one another more seamlessly. This should push the conversation in a more serious direction.

The question is no longer whether Africa can trade more. It is whether Africa can trade upward.

Can it use continental integration not merely to move more goods, but to restructure the nature of the goods being moved? Can it create regional chains in food processing, textiles, pharmaceuticals, automotive components, energy technologies, critical minerals processing, digital services, and construction materials?

Can it build trade corridors that carry not only tonnage but transformation? Can it mobilize African capital behind productive systems rather than waiting endlessly for external salvation?

Export Dignity

Africa does not merely need export growth. It needs export dignity.

Export dignity means that what leaves the continent should increasingly carry knowledge, labor complexity, process sophistication, and premium capture. It means African economies should no longer be structurally useful to others before they become structurally valuable to themselves.

It means a mine should not be treated as the end of the story, but as the beginning of an industrial question. It means agriculture should not terminate at the farm gate.

It means trade policy should not be discussed separately from factory capability. It means ports should become gateways for competitive systems – not conveyor belts of unfinished potential.

The old model made Africa visible but not formidable. It made the continent indispensable in material terms, while leaving it peripheral in strategic terms.

That is why so many economies across Africa have remained vulnerable to external price swings, currency shocks, financing gaps, and imported inflation. Afreximbank estimates Africa’s trade finance gap at approximately US$100 billion annually. That gap is not a side issue. It is part of the machinery through which value-chain exclusion reproduces itself.

When firms cannot access the right financing at the right points in production and trade, they struggle to move beyond lower-value participation.

So Africa’s real export problem is not export volume alone. It is value capture.

And value capture is ultimately about control – over processing, over standards, over payment systems, over industrial policy, over domestic capital deployment, and over the legal, technological, and logistical layers that determine who keeps the thickest part of the margin.

Redesigning What Africa Keeps

For too long, we have spoken as if the mere possession of resources ensures future wealth. It does not. Resources are invitations, not guarantees. They invite strategy or exploitation, sovereignty or dependency, industry or leakage.

If a continent does not organize itself around the upward movement of value, it will watch others organize around it. That is what is happening now.

The world is racing to secure supply chains in energy, technology, food systems, and strategic manufacturing. Africa can either remain the quarry beneath that future or become one of its architects.

But architecture requires intention. It requires a different kind of state, a different kind of capital, a different kind of elite, and a far greater tolerance for the unfinished work of institutional seriousness.

The next chapter of African prosperity will not be written by those who merely celebrate what the continent has. It will be written by those who redesign what the continent keeps.

Because the deepest loss in African economic life is not always the outright theft of resources. Sometimes it is the normalization of exporting possibility and importing dependence.

And that is why the value chain is not just an economic concept. It is a map of power.

Until Africa climbs it with discipline, it will continue to mistake movement for progress and trade for transformation. But the day the continent begins to hold more of the chain, shape more of the process, own more of the premium, and organize more of the capital behind production, something profound will shift. Africa will no longer be known mainly for what it contains beneath the ground or grows from the soil. It will be known for what it builds on top of both.

That is when exports stop being evidence of extraction – and start becoming evidence of civilization.

Daki Nkanyane is a South African – born Pan-African thought leader, entrepreneur, keynote speaker, and strategist with over 25 years of experience driving innovation, identity, and development across Africa. He is the Founder & CEO of Interflex Capital, AfrisoftLive, QonnectedAfrica, and iThinkAfrica, where he focuses on youth empowerment, entrepreneurial ecosystems, and Africa’s economic and ideological renewal. His work spans technology, digital transformation, major international events, and strategic advisory for future-ready African institutions. As a contributing writer for The Habari Network, Daki covers African innovation, leadership, human capital, economics, entrepreneurship, and Africa–Caribbean relations through cultural, philosophical, and developmental perspectives. His mission is to help shape a new African consciousness rooted in pride, possibility, and self-determination for Africans on the continent and in the diaspora. He can also be reached on Facebook and X.