Opinion

Mozambique’s IMF Repayment: A Signal, Not Just a Settlement

By Gregory September

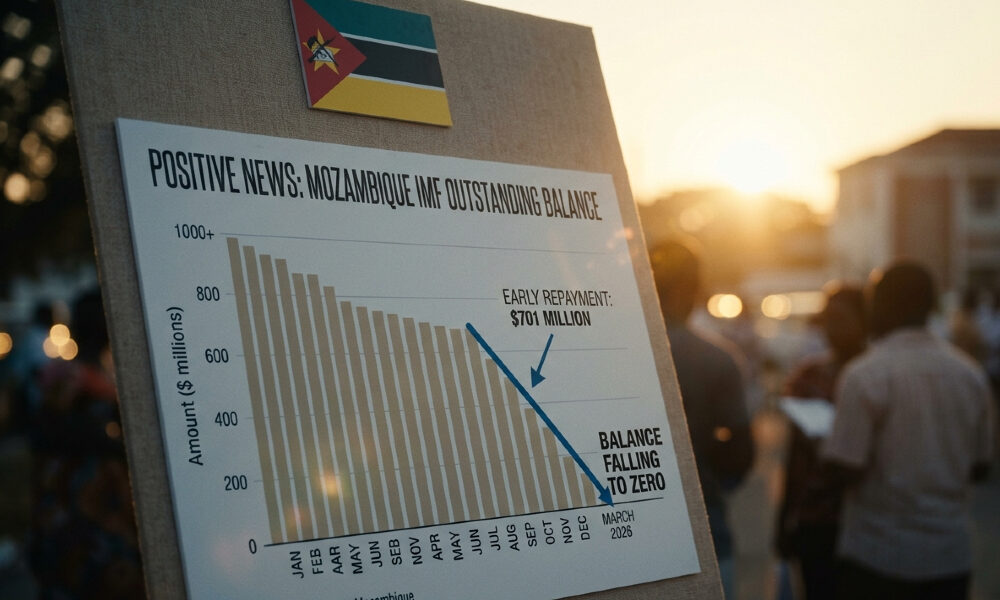

In a continent where sovereign debt rarely shrinks ahead of schedule, Mozambique has done something that 85 countries with outstanding International Monetary Fund obligations have not. It has reduced its IMF balance to zero.

The US$701 million repayment – completed in full, ahead of schedule, without extensions or renegotiation – cleared the country’s outstanding credit under a prior suspended program.

Between March 1 and March 30, 2026, Mozambique’s outstanding IMF balance fell from 514 million Special Drawing Rights to nothing. That is not a rounding error. That is a deliberate act of fiscal policy with consequences that extend well beyond the balance sheet.

What the Numbers Actually Mean

The repayment will reduce Mozambique’s foreign reserves from approximately US$4.15 billion to an estimated US$3.5 billion – a meaningful drawdown that critics have been quick to flag. The concern is legitimate: liquidity matters, particularly for a country that still faces substantial development financing needs and operates in an external environment defined by commodity price volatility.

But the Mozambican government’s reasoning deserves to be taken seriously on its own terms. As officials have noted, early repayment preserves the central bank’s balance sheet and, in turn, its capacity to consolidate macroeconomic stability.

That is not an ideological statement. It is a technical one, grounded in the logic of central bank credibility and the cost of maintaining contingent liabilities on a sovereign balance sheet.

The IMF has confirmed the transaction and indicated that a staff visit is forthcoming. The cancellation of the previously planned August mission reflects the repayment itself – not a rupture in the relationship.

Mozambique continues to pursue a new IMF program aligned with ongoing structural reforms, and technical cooperation between the two parties remains intact.

Sovereignty and the Question of Sequencing

The deeper debate this repayment provokes is not really about Mozambique. It is about the sequencing of financial independence in lower-income economies – specifically, whether exiting IMF program conditions before locking in alternative sources of concessional financing represents strategic clarity or premature confidence.

The IMF’s lending facilities for low-income countries carry below-market interest rates and considerable flexibility. Paying them down early is, in one sense, forgoing cheap capital.

In another sense, it is buying back room to maneuver – the ability to negotiate future programs from a position of demonstrated fiscal discipline rather than accumulated indebtedness.

Rwanda managed a version of this transition. So, in different ways, have Botswana and Mauritius.

The common thread is not ideology but institutional credibility: countries that consistently do what they say they will do acquire a different kind of leverage in subsequent negotiations – with the IMF, with bond markets, and with bilateral partners.

Mozambique is not Rwanda, and the structural challenges it faces are formidable. But the signal being sent here is not that the country no longer needs external support. It is that the country intends to engage that support on its own terms.

Why This Matters Beyond Maputo

Africa’s relationship with multilateral debt has long been characterized by a painful asymmetry: the terms of borrowing are set elsewhere, the conditions of restructuring are set elsewhere, and the political costs of compliance are borne locally. Against that backdrop, a voluntary early repayment by a country that could have quietly allowed the obligation to run to maturity is a meaningful act of agency.

It is not a template that every African government can or should replicate – reserves positions, financing needs, and debt structures differ enormously across the continent. But it does something important to the narrative. It demonstrates that the direction of travel on sovereign debt in Africa is not uniformly toward accumulation and restructuring. Some governments are choosing a different path.

Whether Mozambique’s reserves hold steady, whether the new IMF program is concluded on favorable terms, and whether the macroeconomic gains the government is anticipating materialize – these remain open questions. The transaction does not answer them.

What it does do is place Mozambique in a category occupied by very few of its peers, and invite the rest of the continent to consider why.

The IMF’s door remains open. Mozambique has simply chosen, for now, to stand on the other side of it.

Gregory September is a South African academic, author, and geopolitical analyst with extensive experience in government and Parliament. He is the founder and CEO of SAUP (Sustainability Awareness and Upliftment Projects NPC), which focuses on sustainability education and community development. He previously served as Head of Research and Development for the Parliament of South Africa. His work centers on sustainability, African geopolitics, and economic development, and he regularly contributes to analysis of global political and economic affairs.