Opinion

Africa’s Growth Is Real But Uneven: What Its Fastest-Growing Economies Reveal

By Des H Rikhotso

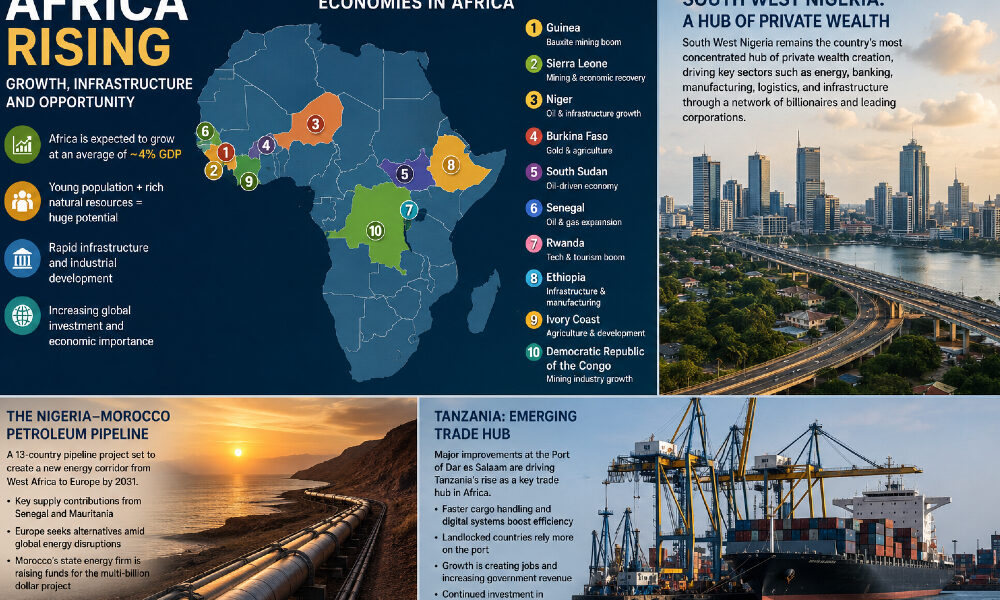

Africa’s economic narrative is often reduced to clichés of either limitless promise or structural stagnation. The reality, as ever, is more complex – and far more interesting. Across the continent, pockets of rapid growth are emerging, driven by commodities, infrastructure expansion, demographic momentum, and selective diversification into services and manufacturing.

Africa’s Fastest-Growing Economies: Resource Wealth Meets a Rising Generation

From Guinea’s bauxite fields to Rwanda’s technology corridors, a diverse set of growth drivers is reshaping the continent’s economic landscape – and demanding the world’s attention.

Projected average GDP growth

Fastest-growing economies ranked

Population under age 25

Africa is not merely growing; it is recomposing. Across the continent, a cohort of economies is expanding at rates that would have seemed implausible a decade ago, powered by a convergence of commodity booms, demographic advantage, and – crucially – a new generation of public and private infrastructure investment.

The continent’s median age of roughly 20 years is not a demographic footnote – it is an economic argument. A young, urbanizing labor force, combined with rapidly deepening digital connectivity, creates the conditions for the kind of compounding productivity gains that transformed East and Southeast Asia in the late twentieth century.

“Africa’s median age is an economic argument, not merely a demographic footnote.”

The ten economies leading this charge span the continent in geography and growth model alike.

| 1 | Guinea | Bauxite mining expansion |

| 2 | Sierra Leone | Mining and post-conflict recovery |

| 3 | Niger | Oil production and infrastructure |

| 4 | Burkina Faso | Gold output and agricultural growth |

| 5 | South Sudan | Oil-driven fiscal expansion |

| 6 | Senegal | Oil and gas sector development |

| 7 | Rwanda | Technology services and tourism |

| 8 | Ethiopia | Industrial manufacturing and logistics |

| 9 | Ivory Coast | Agricultural exports and urban development |

| 10 | DR Congo | Critical minerals and mining |

What distinguishes this cycle from previous African growth spurts is the breadth of the drivers. Rwanda’s ascent rests on governance reform, technology investment, and premium tourism – not a single commodity. Ethiopia has pursued an industrial-park strategy modeled loosely on China’s special economic zones.

Ivory Coast has deepened agricultural value chains rather than simply exporting raw cocoa. These are structural stories, not commodity luck.

That said, resource dependence remains a salient risk. Niger, Burkina Faso, and South Sudan remain heavily exposed to the volatility of global commodity markets and, in several cases, to fragile political conditions. Sustained growth at the continental average of roughly 4 percent annually will require governance improvements, intra-African trade expansion under the African Continental Free Trade Area, and the patient build-out of power, roads, and digital infrastructure.

The potential is unambiguous. The path, as ever in Africa, is the harder question.

Nigeria

Southwest Nigeria: The Quiet Engine of West Africa’s Largest Economy

Lagos and its hinterland continue to concentrate Nigeria’s private wealth – a dominance that reflects both the region’s strengths and the structural imbalances of a continent-sized federation. In the geography of Nigerian capitalism, the southwest occupies a position analogous to that of California in the American economic imagination: outsized in its wealth, disproportionate in its corporate influence, and increasingly indispensable to the national story even as the federation officially insists on balance.

As of 2026, the region anchors Nigeria’s most consequential private-sector activity. Its billionaire class commands conglomerates whose combined annual revenues run into the tens of trillions of naira – a figure that, while difficult to pin down with precision, is broadly consistent with the concentration of Nigeria’s high-net-worth individuals that independent wealth surveys have documented in recent years.

“In the geography of Nigerian capitalism, the southwest occupies a position analogous to California in the American economic imagination.”

The sectors that define the region’s influence are telling: energy, commercial banking, manufacturing, logistics, and infrastructure. These are not glamorous, disruptive industries – they are the unglamorous load-bearing columns of a modern economy.

That the southwest hosts their headquarters and their decision-makers speaks to decades of accumulated institutional advantage: the deepest port, the oldest universities, the most developed professional services ecosystem on the West African seaboard.

The risk, acknowledged privately by many Lagos-based executives, is that this concentration breeds complacency in the city and resentment beyond it. Sustained national growth requires the distributed development of other regions – the north, the southeast, the Niger Delta – not merely the continued enrichment of an already-dense southwestern hub.

Whether federal policy in 2026 is moving meaningfully in that direction remains, to put it charitably, debatable.

Energy Geopolitics

The Nigeria-Morocco Gas Pipeline: A New Energy Corridor Emerges at Europe’s Peril of Inaction

As geopolitical shocks disrupt established supply routes, a trans-West African pipeline project offers Europe a chance to diversify – if the financing and the politics can be aligned in time. Energy corridors, once built, tend to outlast the political circumstances of their construction by generations.

The Nigeria-Morocco Gas Pipeline, currently advancing through feasibility, financing, and diplomatic negotiation, may prove to be the defining infrastructure project of West Africa’s energy decade – and one of Europe’s most consequential import decisions of the 2030s.

The project’s ambition is considerable. Spanning 13 countries along the Atlantic coast of Africa – with meaningful supply contributions expected from Senegal and Mauritania, whose offshore gas fields are among the most significant recent hydrocarbon discoveries on the continent – the pipeline is designed to deliver West African gas to European markets by approximately 2031.

Morocco’s state energy company is now in the early stages of raising the substantial capital the project requires.

“Energy corridors, once built, tend to outlast the political circumstances of their construction by generations.”

The geopolitical rationale has sharpened considerably in recent months. Disruptions in the Strait of Hormuz and the resulting energy price surges have reanimated European anxieties about import concentration – anxieties that were already acute following the realignment of Russian gas flows after 2022.

A reliable, long-term Atlantic supply route from West Africa would meaningfully reduce Europe’s exposure to both Middle Eastern and Russian price shocks.

The obstacles are formidable. Financing a multi-billion-dollar pipeline across 13 jurisdictions, many of them characterized by variable governance and regulatory uncertainty, is an undertaking that has defeated less ambitious projects. Security conditions along portions of the route, particularly in the Sahel, introduce additional complexity.

And the pace of Europe’s energy transition, if accelerated by policy ambition, could theoretically reduce the long-run demand for the gas this pipeline is designed to deliver.

Yet the project’s proponents have logic on their side. The energy transition will not be instantaneous, and baseload gas will remain part of the European mix well into the 2040s.

A diversified import portfolio – one that includes West African supply rather than depending on a handful of existing corridors – is not contrary to European energy security; it is the definition of it.

Trade Infrastructure

Tanzania’s Port of Dar es Salaam: From Bottleneck to Gateway

Decades of congestion have given way to measurable efficiency gains, transforming the port into a linchpin of East and Central African trade – though the work of sustaining that transformation has only just begun.

Ports are not glamorous. They are, however, among the most consequential pieces of physical infrastructure a developing economy can possess – multipliers of trade, generators of employment, and, when they function well, magnets for the regional commercial activity that landlocked neighbors cannot access on their own.

The Port of Dar es Salaam has spent much of its recent history as a cautionary example of the opposite: a chronically congested facility whose delays imposed measurable costs on Tanzanian exporters and, more damagingly, on the landlocked economies – Zambia, Rwanda, and the Democratic Republic of Congo, among others – that depend on it as their primary conduit to global markets.

“Ports are multipliers of trade — and when they function well, magnets for regional commercial activity that landlocked neighbors cannot access alone.”

The turnaround, when it came, was the result of a coordinated combination of infrastructure investment, digital systems modernization, and customs process reform. Cargo handling speeds have improved materially. Turnaround times have declined. And the knock-on effects – increased trade volumes, rising government revenue, and a measurable strengthening of Tanzania’s position as the region’s primary transit hub – are now visible in the data.

Crucially, the landlocked neighbors are noticing. Zambia, Rwanda, and the DR Congo have deepened their logistical reliance on Dar es Salaam, a shift that is both commercially rational and geopolitically significant. Tanzania’s emergence as a genuine East African trade hub gives it leverage, influence, and – if managed well – a durable revenue stream from transit fees and port services.

The risks are familiar to students of African infrastructure. Efficiency gains achieved through targeted investment can erode quickly if follow-on funding for road and rail links connecting the port to the interior is not secured.

The port’s hinterland connectivity remains the critical variable. Tanzania has demonstrated, creditably, that it can reform a major piece of logistics infrastructure.

The harder test – sustaining and extending those reforms against the competing pressures of politics and budget constraint – lies ahead.

Des H Rikhotso is a seasoned C-Suite Multi-Industry (Automotive – OEM + Retail, Logistics, Oil & Gas, etc) business executive with 25+ years of Business Leadership Experience across the South, East and Western Sub-Sahara Africa Region. Based in Kampala, Uganda he serves as East Africa Region Country Director and Business Executive, driving Business Strategic Growth and Operational Excellence – contributing his Business Leadership Experience to the Region. Des has held Business Leadership roles at BMW Group Africa, Volkswagen Group Africa, Peugeot Motors South Africa, Toyota/Lexus South Africa, Lexus East Rand (Unitrans/CFAO), Nissan Group of Africa, G.U.D Holdings (Africa Exports Operations Division),The HDR Group of Companies and The Ezra Group of Companies (a Leading Uganda & East Africa Conglomerate). He holds Under-Graduate and Post-Graduate business degrees from the University of the Western Cape, Wits University (Wits Business School) and the University of South Africa.