Business

Africa’s Energy Mosaic: A Strategic Blueprint for Investment and Transition

By John Kourkoutas

Africa is not a monolith – and nowhere is this truer than in its energy sector. A continent often mischaracterized as uniformly underpowered is, in fact, a dynamic patchwork of energy ecosystems, each with distinct advantages, vulnerabilities, and transition pathways.

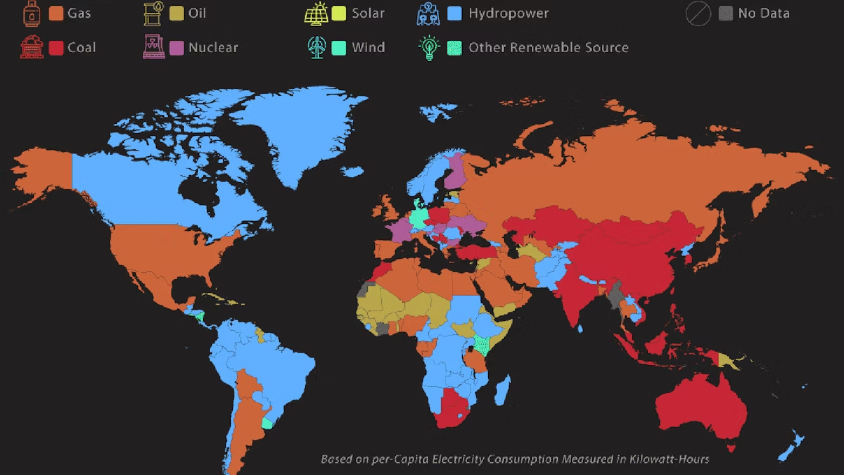

A new global energy sources map – color-coded by dominant generation type – reveals not just where power comes from, but where the next decade’s most compelling economic and strategic opportunities lie.

- (Blue) Hydropower: Dominant in East and Central Africa – renewable, low-cost, but climate-sensitive.

- (Orange) Natural Gas: Prevalent in West Africa – serving as a transitional bridge, yet increasingly pressured to diversify.

- (Red) Coal: Concentrated in Southern Africa – high-carbon, costly to maintain, and under mounting regulatory and environmental scrutiny.

- (Yellow) Solar: Emerging rapidly in North Africa – ideal conditions, underutilized potential.

- (Purple) Nuclear and (Cyan) Wind: Niche but growing, signaling advanced infrastructure ambition in select markets.

This isn’t just an energy map – it’s an investment compass.

The Real Story Behind the Colors

Having worked across more than 24 African countries, I have seen firsthand how energy mix dictates not only environmental outcomes but economic competitiveness. Energy isn’t a back-office concern; it’s a frontline determinant of operational cost, carbon exposure, and long-term viability.

- Hydropower-rich nations like Ethiopia, Zambia, and the Democratic Republic of Congo offer some of the lowest electricity tariffs on the continent – often 80 percent lower than coal-dependent peers. But they are vulnerable to droughts and climate volatility, demanding hybrid solutions (solar + wind + storage) to ensure reliability.

- Gas-reliant economies in West Africa – Nigeria, Ghana, Senegal – are at a crossroads. While gas provides baseload stability today, policy momentum and investor pressure are accelerating the pivot toward renewables. The window for gas-to-renewables integration is open – but narrowing.

- Coal-heavy systems in South Africa and Zimbabwe face existential pressure. Stranded asset risks are rising, and the cost of retrofitting or replacing aging plants is staggering. Yet this creates a massive infrastructure opportunity: grid modernization, renewable retrofits, and just transition financing.

- North Africa’s solar belt – from Morocco to Egypt – boasts some of the world’s highest solar irradiance. Yet deployment lags behind potential. With falling technology costs and rising demand for green hydrogen and data centers, the region is primed for exponential growth.

Where the Opportunities Lie

For renewable energy firms:

- Deploy hybrid microgrids in hydropower zones to buffer climate risk.

- Scale utility-scale solar in North Africa with integrated storage.

- Partner with West African utilities to design gas-to-renewables transition roadmaps.

For industrial and tech investors:

- Site energy-intensive manufacturing – aluminum smelting, green hydrogen, data centers – in hydropower corridors. The DR Congo, Ethiopia, and Zambia offer not just cheap power but strategic access to growing markets.

- Avoid “carbon traps”: locating in coal-dependent grids can inflate both costs and ESG risk – sometimes by 300 percent or more compared to hydro zones.

For infrastructure developers:

- Prioritize grid interconnectivity between hydro-rich and solar-rich regions.

- Invest in modular, decentralized solutions for areas lacking dominant generation – especially in the Sahel and Central Africa.

- Build energy storage capacity where renewables are scaling but grid flexibility is limited.

The Bottom Line

The winners of Africa’s next growth wave won’t be those who treat the continent as a single market. They will be the ones who read the map – who understand that energy infrastructure shapes everything from supply chains to sustainability ratings.

Your choice of location isn’t just logistical – it’s strategic. Your carbon footprint isn’t just ethical – it’s financial. Your energy reliability isn’t just technical – it’s existential.

Africa’s energy transition isn’t a distant promise. It’s unfolding now – and the map shows exactly where to act.

Ask yourself: Which energy ecosystem dominates your target market – and how will that shape your competitive edge?

John Kourkoutas is business development expert that specializes in helping companies, export teams, and business leaders succeed in Africa’s dynamic and emerging markets.